- All Posts

- Automation

- Cashflow

- Compensation

- Compliance

- Cost Cutting

- Employees

- Expenses

- Fraud

- Health Insurance

- Healthcare

- Hiring

- Privacy

- Savings

- Security

- Taxes

- Technology

- Testimonials

May 4, 2026/

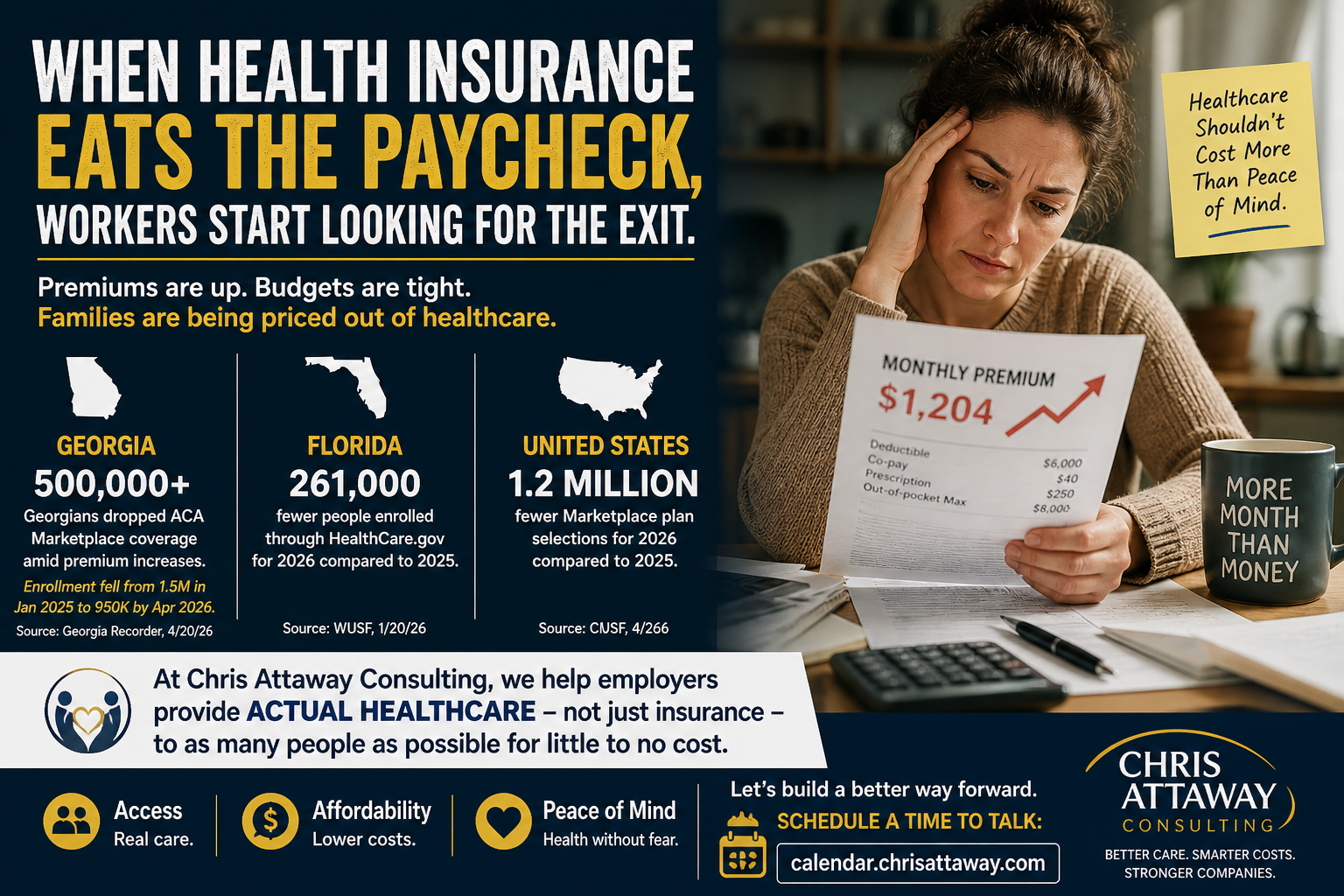

For decades, employer-sponsored health insurance has been treated like the gold medal of employee benefits. Get the job. Get the...

April 28, 2026/

A Quiet Rule Change That Could Have Loud Consequences Most business owners don’t wake up thinking about Department of Labor...

November 10, 2025/

UnitedHealthcare plans 11 premium hike for 2026 but employers finally have a better option It’s official: UnitedHealthcare has announced...

October 10, 2025/

The numbers are in, and they’re not pretty: According to the latest KFF Health Benefits Survey,the average cost of family...

September 10, 2025/

Lower Costs. Increased Profits. Happy Employees.If you’re like most employers, your benefits costs feel like they’re on autopilot—rising every year...