For decades, employer-sponsored health insurance has been treated like the gold medal of employee benefits.

Get the job. Get the benefits. Keep the benefits. Be grateful.

That was the deal.

But lately, more employees are looking at their paychecks, looking at their premiums, looking at their deductibles, and quietly asking a dangerous question:

“What exactly am I paying for?”

And that question should make every employer sit up a little straighter.

A recent article highlighted a growing trend: healthy workers are beginning to walk away from expensive company health plans because the monthly cost no longer makes financial sense for their families. One family mentioned in the article saved nearly $1,000 per month by leaving the employer plan and choosing a different option.

That is not pocket change. That is a mortgage payment. A car payment. Groceries. Debt reduction. Breathing room.

And right now, breathing room is in short supply.

The Benefit Employees Can’t Afford Is Not Really a Benefit

The average annual premium for employer-sponsored family coverage reached $26,993 in 2025, with workers contributing an average of $6,850 toward that cost. Family premiums rose 6% in 2025, and they are up 53% since 2015, according to KFF.

Let that sink in.

A family health plan now costs almost as much as a small car every single year.

And many employees are not only paying premiums. They are also facing deductibles, copays, coinsurance, out-of-network surprises, prescription costs, and the soul-crushing experience of calling an insurance company and hearing, “Your call is important to us.”

That phrase has personally aged America by at least seven years.

The problem is not that employers do not care. Most employers I speak with absolutely care. The problem is that the system has become so expensive and complicated that even good employers are often stuck offering benefits that look impressive on paper but feel painful in real life.

Healthy Workers Are Doing the Math

The uploaded article makes an important point: the workers most likely to leave expensive plans are often young, healthy employees.

That matters.

Traditional insurance depends on a balanced risk pool. Healthy people pay in. Sicker people use more care. The plan survives because the pool is broad enough to absorb the cost.

But when healthy employees start opting out, the plan can become more expensive for everyone who remains.

That is the beginning of a bad cycle:

Healthy workers leave because the plan costs too much.

The remaining group gets more expensive.

Premiums rise again.

More workers question the plan.

Employers get hit at renewal.

Employees blame the employer.

HR gets trapped in the middle, armed only with a spreadsheet and a forced smile.

That is not a benefits strategy. That is musical chairs with a billing department.

This Is Bigger Than One Company

This pressure is not limited to employer-sponsored plans.

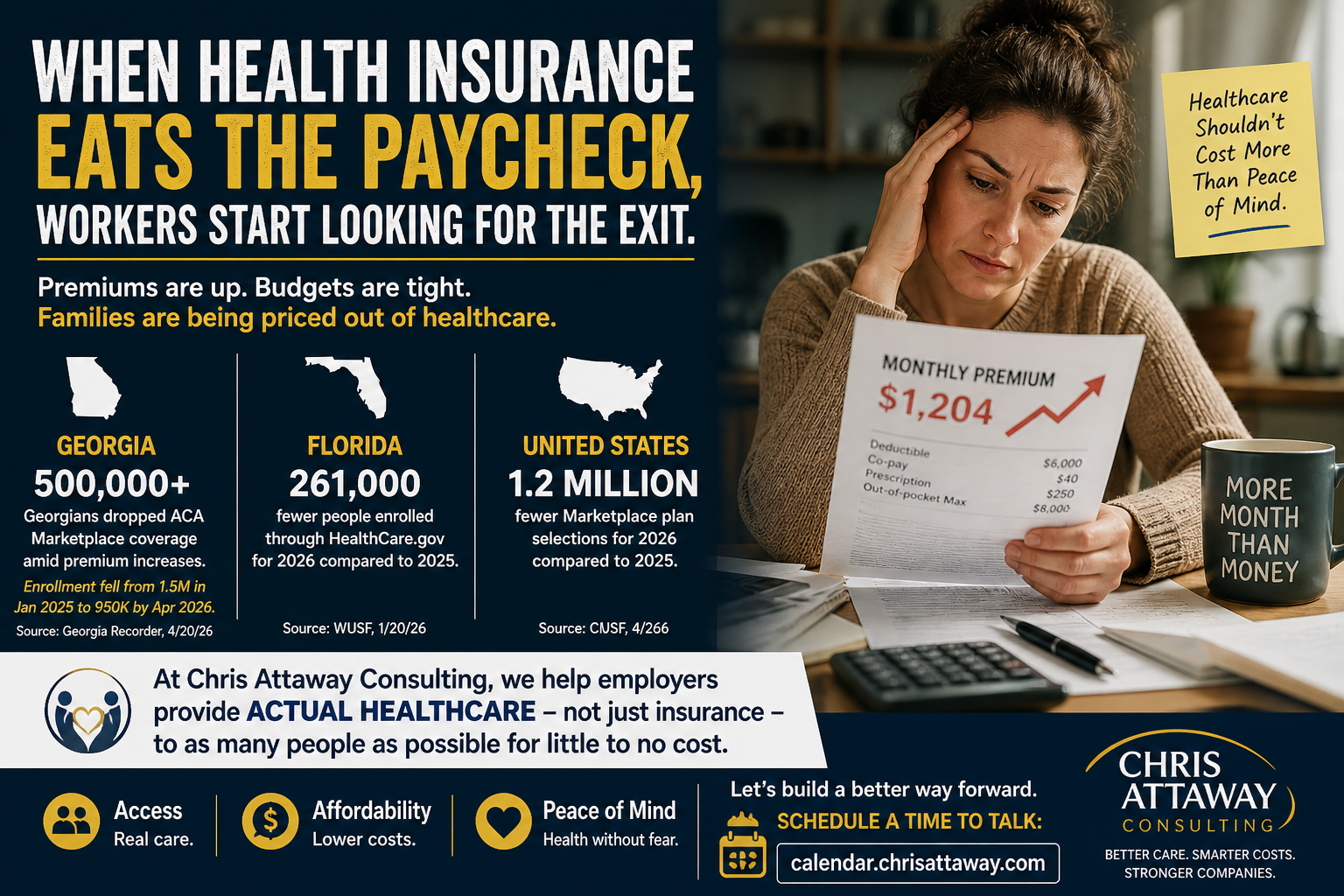

In Georgia, more than 500,000 people reportedly dropped ACA Marketplace coverage amid steep premium increases, with enrollment falling from roughly 1.5 million in January 2025 to 950,000 by April 2026.

In Florida, about 261,000 fewer people enrolled through HealthCare.gov for 2026 compared with 2025.

Nationally, CMS reported 23.1 million Marketplace selections during the 2026 open enrollment period, about 1.2 million fewer than the previous year.

People are not walking away because they suddenly stopped needing healthcare.

They are walking away because insurance is becoming unaffordable.

That is the key distinction.

People still need doctors. They still need prescriptions. They still need mental health support. They still need help when a kid wakes up with a fever at 2 a.m.

What they do not need is another expensive card in their wallet that they are afraid to use.

Employers Need a New Conversation

Most benefit conversations are still built around insurance.

What is the premium?

What is the deductible?

What is the network?

What is the renewal?

Those questions matter. But they are not enough.

The better question is:

How do we give employees more actual access to healthcare while putting more money back in their pockets?

That is where Chris Attaway Consulting comes in.

We help employers address the real-world problem underneath the insurance problem. Employees do not simply need “coverage.” They need care they can actually use.

That means access to things like doctors, mental health support, prescriptions, and everyday healthcare services in a way that can be provided for little to no net cost when structured properly.

This is not about replacing every existing benefit plan or asking employers to blow up their current vendor relationships. It is about adding a smarter strategy alongside what is already in place so employees can get more help, employers can reduce unnecessary cost pressure, and both sides can stop pretending that higher premiums are just a normal part of life.

Because they are not.

They are a warning light.

And when the warning light comes on, you do not solve it by putting tape over the dashboard.

The Employers Who Move First Will Win

The companies that figure this out early will have a serious advantage.

They will recruit better.

They will retain better.

They will give employees something they can feel immediately.

They will also have a better answer when workers say, “I can’t afford this anymore.”

Because that day is coming for more businesses.

For some, it has already arrived.

If your employees are struggling with the cost of healthcare, or if your renewal feels like a hostage negotiation with nicer fonts, let’s talk.

Schedule a quick appointment with me here:

calendar.chrisattaway.com